4 Innovative FinTech Apps that Changed Digital Banking in Hungary

When the first microchips were created, no one assumed that the IT industry would invade the markets of almost every sector. The 21st century saw an acceleration of this trend with the advent of Fintech in addition to a number of other changes. The intertwining of the financial and technology industries is not merely a necessity in the era of constant efficiency improvements and cost cutting measures, but also a new opportunity to familiarize users with new convenience services never seen before.

Let's be honest, laziness (or the pursuit of comfort, if you wish) is a serious motivational factor for most people. Companies involved in the Fintech industry have recognized this factor and are nowadays challenging the big players who are slow to react due to their locked-in market position. The Fintech segment, mostly perked up by startups, is trying to lure the users from the big and powerful players of the financial market.

Despite the delay, the traditional financial sector has recognized the importance of Fintech and started to catch up. So the most recent developments come not only from startup companies but also from the big and powerful players who want to prevent the loss of their users.

However this process does and will certainly have some victims as well. Despite the fact that financial markets will continue to grow in the magnitude of tens of billions, based on Citigroup's forecast, it is possible that the number of jobs within the financial sector will decrease by as much as 30 percent over the coming years. Namely, most of the investments are spent not on creating new jobs, but on further developing, customizing and applying these booming technologies such as artificial intelligence, machine learning, deep learning, etc.

Millions of possibilities

One of the best known Fintech stories is the crypto currencies, in particular, such as Bitcoin. While behind every national currency there is always a country that values creating strength of which gives a certain level of safety in terms of the acceptance and use of the money, this trust comes from a very different place in case of the crypto currencies(which trust is far less stable than in the case of euros or dollars). The value and the capitalization of the Bitcoin, supported by an encryption process, distributed calculation capacity and anonymity, increased substantially in just a few years, and the exchange rate of just a few dollars cents climbed up to $4,000 by the middle of 2017.

It is clearly apparent that investing at the right time and at the right place can bring huge returnsin just a couple of years. But most of the Fintech services have a more modest growth, their significance comes from the innovation they offer. Such as, for example, Koin, the financial application of MagNet Bank,which is able to track the user’s spending through mobile phone. This mobile application was developed based on the needs of the users for a simple and fast tracking and administration of their spending. No wonder the app received a rating of 4.5 in Google’s app store, Google Play, and was downloaded by more than 50,000 Hungarian users. With the help of this application the user can precisely know at all times how much they spent on what, making their spending more transparent. The application keeps track of their incomes and expenses and when connected to the banking system, it can do this automatically, without any manual intervention.

The interface of Koin

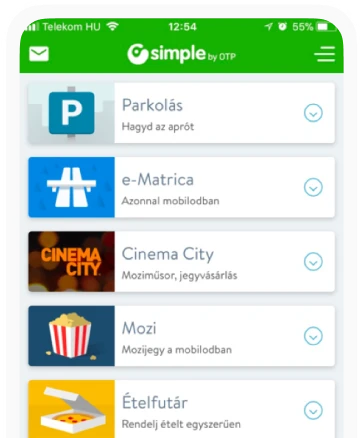

The interface of KoinAnother popular Fintech solution developed in Hungary is the Festipay Prepaid MasterCard which had its debut on last year's Sziget Festival. An important feature of this payment card is that it can be used only up to the amount prepaid on the card, but can also be used for online purchases. OTP’s Simple application is also popular, planned and tested by Ergománia has been already downloaded by more than 250 ,000 users. This card can be used for buying parking tickets, motorway stickers and for ordering food, among other things. What is more, you can even digitalize your bank card with the help of this application, meaning that you can use your mobile device suitable for contactless mobile payment as a bank card. Simple app won the first prize of the most user-friendly fintech application. In its evaluation, the jury highlighted its practical features and simple usability. No wonder, since a clearly understandable, user-friendly interface meeting users’ expectations is especially importantfor newly introduced applications.

It is true for every interface, but especially for these, that the interface must be well adapted to the users’ conscious and unconscious expectations and mental models. Applications of these types cannot be developed without preliminary research and constant testing throughout the development stage. If these aspects are neglected, bugs are bound to occur after its release and parts of the development must be restarted from scratch. Or worse, the existing application must be patched again and again.

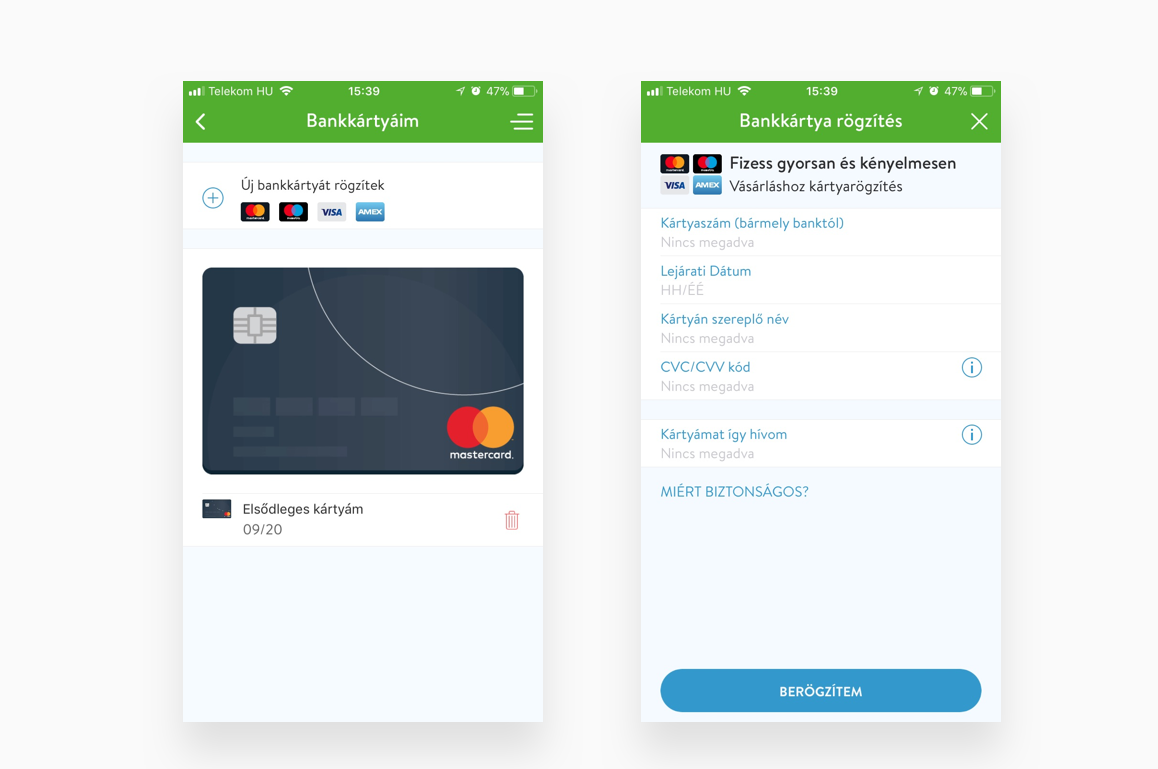

The interface of Simple

The interface of SimpleErgomania tested the application based on user statistics. The figures show that the parking and food ordering were the most frequently used functions, therefore the research mainly focused on these. Thereafter the almost finished application was once again tested with the previous and new users.

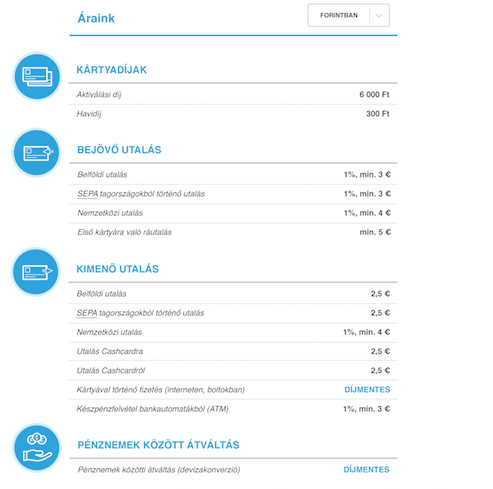

Another innovation for debit cards was CashCardby Peak. CashCard provides bank independent card service with which transactional expenses can be significantly reduced. Moreover, we are allowed to top up our card simply online. Ordering a CashCard is a simple process which can be done purely online.One (and from the user’s point of view probably the most important) part of the website’s design concepts was to create aview of information about the expensesaccompanied by using the service. All expenses aregrouped by activity type and by planseparately.

The interface of Cashcard

The interface of CashcardUnlike the common way of banks, here,allexpense components that are accompanied with card usage are listed separately, without exception. This means that there are no hidden fees, everything is transparent, so potential customers can make sure that they will have to pay not even one penny more than the price written on the webpage. As a consequence, people are not only able to have a quick overview of the site’s content but this kind of behaviour also builds trust in the user and make them feel secure.

Labelingis also worth mentioning. As most of us have the experience with legal texts, financial field also has itstechnical vocabularywhich ordinary people can’t comprehend. Using lingo which is only understood by the ones who apply it every day, in a website for ordinary people makes navigation extremely difficult, increases the cognitive load and hinder users from using the service in general. Besides, easy and quickly fillable forms, easy top-up and the well organized, clean interface in general have a good impact on excellent user experience.

One more relevant issue was the registration process. It was created to make the process efficient and quick since registration is always an additional hurdle for users and thus the faster it is the better. This was achieved by using a simple and clear language which minimised all the misunderstandings by applying additional explanatory lines, where it was necessary.

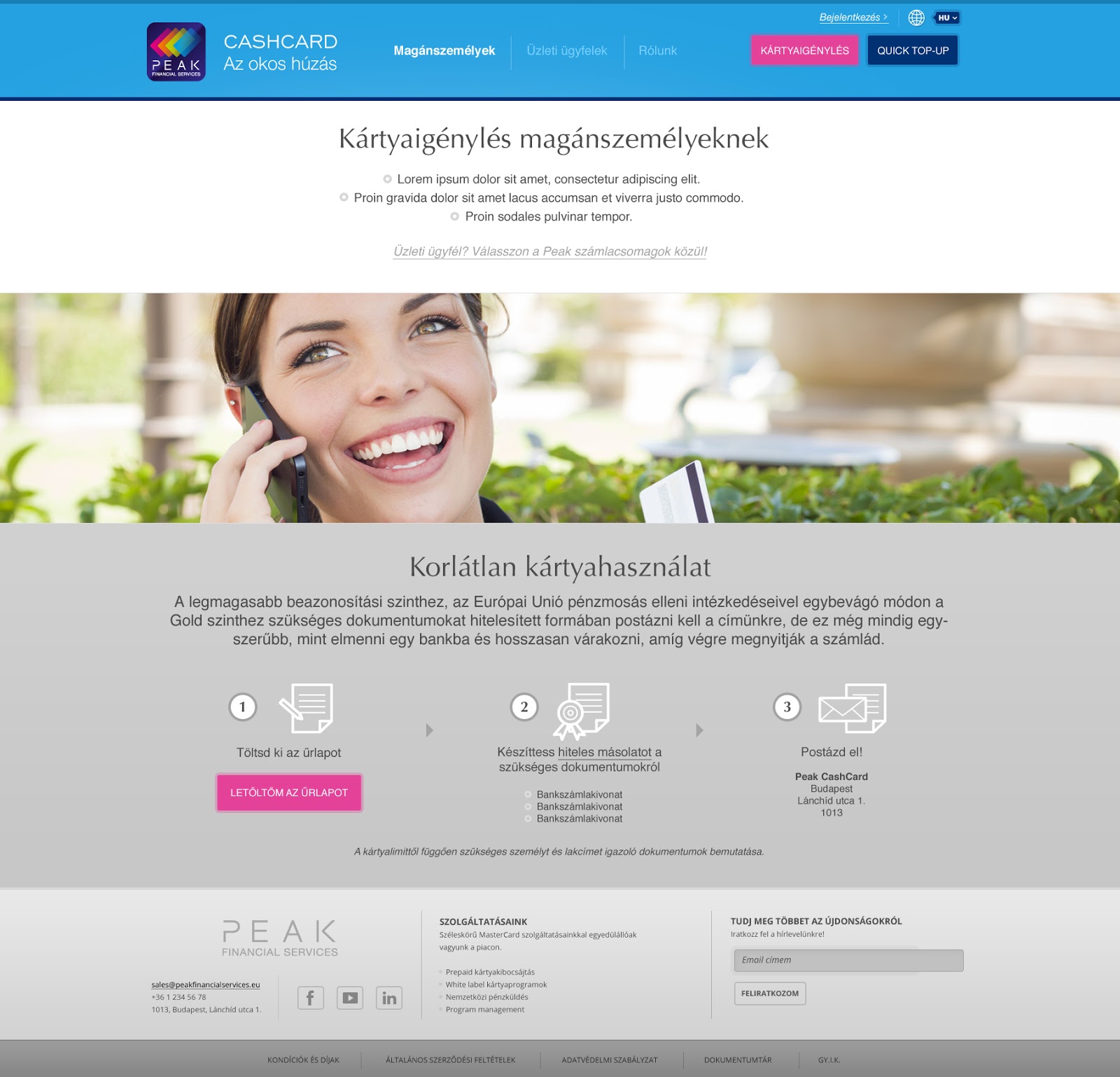

The website of Cashcard

The website of CashcardTo sum up, we can say that FinTech applications, beside providing an alternative to traditional bank solutions, also urge users to innovate and this tension between the two actors on the market ensures constant improvement in the field.

Dr. Csilla Herendy and Anna Régeni are the other contributors of this article.

About the authors

IT expert-journalist with two decades of experience in journalism at Chip Magazin, Terminal.hu, Computerworld.hu and Bitport.hu. Accomplished in modern IT and consumer marketing with thorough posts focusing on the newest trends.

Related posts

A Must-Download for Forward-Thinking Fintech Enthusiasts interested in UX and Digital Payment solutions

In today's rapidly evolving fintech landscape, staying ahead of the curve is not just an option; it's a necessity. This White Paper is an essential read for anyone seeking to gain a deeper understandi...

The Romanian Fintech scene - Trusting your feet

What is a bank for? Why are there bankers? Where is this coming from?I am plunged straight into philosophy by the Co-Founder and CEO of Finqware, one of Romanian Fintech’s brightest offerings. Perhaps...

Fintech conquers Belgium - switching bank accounts service providers automatically and interoperability - part 2

‘If you can’t beat them, join them’ as the old saying goes, which continues to be valid even in the age of Fintech. ING Belgium is attempting to exploit opportunities for rapid financial growth with t...

Related case studies

Percapita

We designed a full-fledged application for simplifying everyday finances.

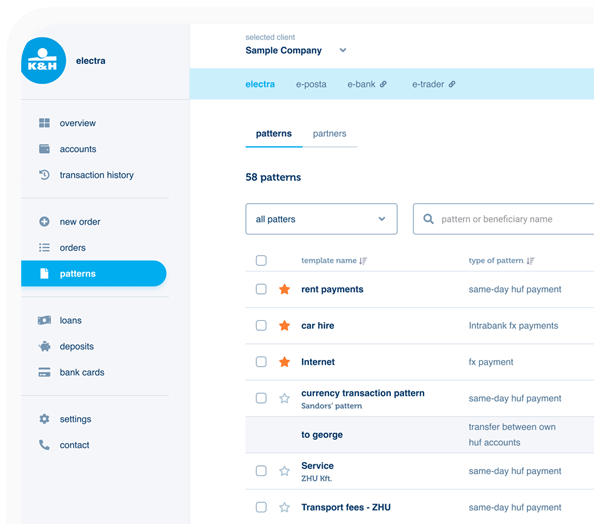

K&H Bank's Corporate Netbank

The K&H Electra Netbank App consolidates all financial needs into a single, user-friendly application. With its intuitive design, businesses can effortlessly manage their company's cash flow, transactions, and investments from one centralized hub.

Atmen Fintech

Mobile App

Designing a Minimum Viable Product for a Diaspora Neobank Startup

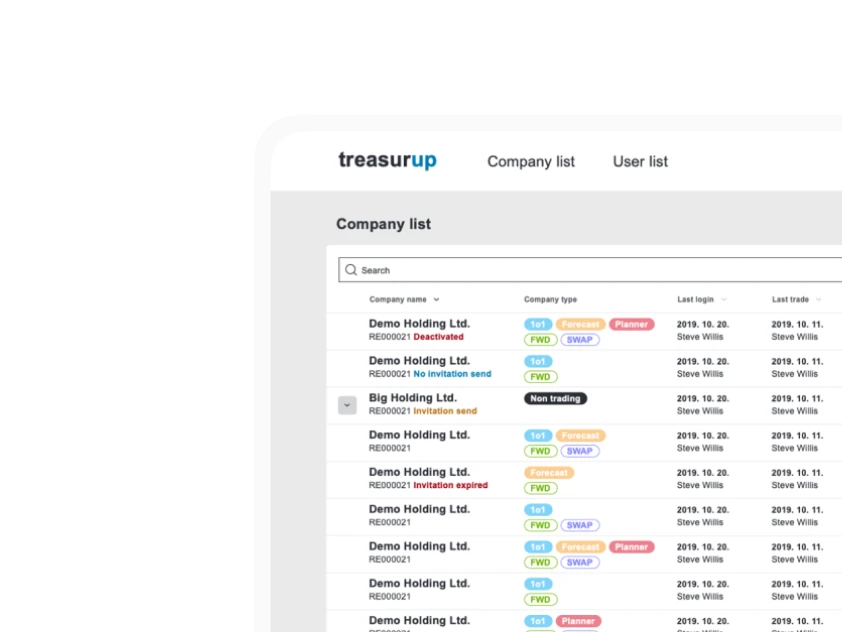

Treasureup

We established written and visual consistencies and guidelines for TreasurUp’s financial platform.

Simple by OTP

Simple by OTP Bank is Hungary's No.1 mobile payment app for cashless payments with 1M+ downloads, and 1 million+ transactions.

White Label Banking App

We provide full-blown next-generation mobile banking solutions for sales-oriented banks.

Want to read more

about UX, fintech and banking?

Subscribe to our biweekly newsletter and get the latest of our news and thoughts!