Smartwatch applications for Fintech

Since the introduction of the first AppleWatch, fintech applications are present for smartwatches, for instance, fintech applications developed for brokers and investors to help them greatly in monitoring and following constantly the change in stock and rate fluctuations without making them take out their phones from their hip-pocket in every 10 seconds.

In present days bank sector is also attempting to catch up with fast technological progress , since by this time it’s practically a must to be able to manage our banking issues purely online. What is even more important is having real-time data and information about our transactions and balances.

By the way, this expectation is the catalizator of the Internet of Things wave as well, since by using the Internet, awful lot of data have been generated and stored and these were utilised to create more personalised advertisements and user experience. So, finally we have come to the point, where we are expecting effective operation of the system in exchange for our data, we are providing our data only if we get something in exchange. In practice, this means that in exchange for the enormous amount of data we provide from ourselves we are expectingtime.We are doing this by expecting from the application to utilise our previously given data to speed up processes and learn from our behaviour.

In essence, this is what learning algorithms and predictive text entry as well as the NEST thermostat are about. NEST learns nice and slowly what are our heating-cooling habits and learns what temperature we keep usually in the different areas of the house.

Basically, in each case, we expect comfort and time efficient operation in return for the data we are providing about ourselves. Returning to the fintech applications, there is a tremendous opportunity in modernising financial processes, because the bank sphere is changing very slowly and reluctantly due to its size, strict rules and clumsiness.

By the appearance of fintech applications and the need for more transparent financial processes, giant banks that are circumvented by these fintech startups must renew their own system, otherwise their downfall is guaranteed. Fortunately, most banks have already come to this conclusion.

There is almost no bank that does not have netbank and mobile bank services to make their customers’ lives easier and prevent them from standing in long queues. Besides, they are saving a lot of money by not maintaining a constant personal customer service with a high number of employees.

A few examples of innovative mobile applications out of the bank sector

In these days, chatbots are becoming more and more popular. These are programmes with the help of which we can easily communicate practically with the service itself. This is much more interactive and in many cases much simpler than go to a webpage and find a particular information there. For instance, there is such a chatbot service which allows you to take out insurance by only chatting with the bot. Such service is Lemonade.

Although Lemonade and taking out insurance are not part of Fintech in the narrow sense but its appearance also shows the innovative tendency of applications and solutions these days. For example, the Cleo app’s creator also has ridden this wave. Its platform is Facebook Messenger; through this platform we are allowed to send money to any of our Facebook friends, check our expenses even from multiple bank accounts with optional filtering alternatives. Moreover, based on our expense and income profile it also helps us save money, which function can be automated by Cleo with an automatically adjusted amount of money that is affordable for the user.

The most popular buzzword among fintech applications is transparency. These quickly proliferating startups are advertising their own applications by telling us that these are much more transparent than traditional bank processes. From the user’s point of view, this means that although they share the same amount of data with the app as they would in the traditional bank setting, nevertheless sharing this data with fintech apps accompanied with benefits for the users as well. How, exactly? On one hand, users don’t have to give their data multiple times, entering and complete transactions can happen by simple fingerprint reading or online entering and at the same time they are often safer than their traditional counterparts since these kind of authentications are more difficult to be hacked.

Smartwatches in Fintech

While mobile banks are equipped with approximately the same functionalites, as their website version, their smartwatch counterpart – because of their limited screen space – usually has only a strongly filtered set of functions. One other reason for this is that most of the time these smartwatch applications also have a mobile application version as well, these two are synchronized and in reality, the smartwatch app only serves as an extended part of the original mobile application that displays only the most relevant and crucial information.

At present, smartwatch applications within the bank sector generally know two-three things: displaying the last few transactions –although almost the same functionality is provided by sms notification, except that it is vibrating in your pocket and not on your wrist, moreover, they usually also display close ATMs and your balance, even from multiple bank accounts.

iBank. Resource: https://www.banksa.com.au/online-services/wearables

iBank. Resource: https://www.banksa.com.au/online-services/wearables

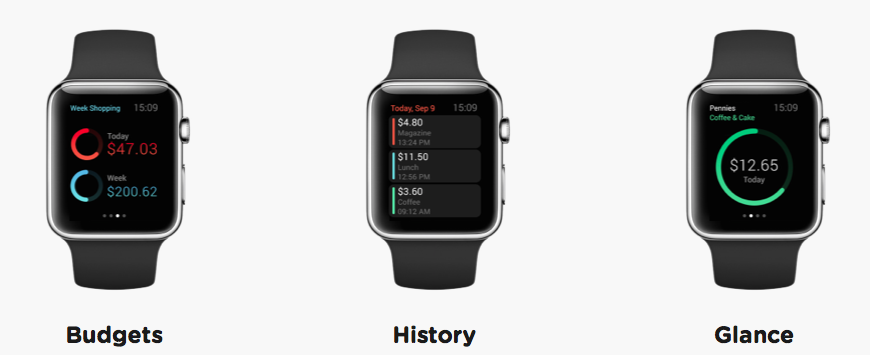

Nevertheless, there are Fintech applications out of the bank sphere as well and usually the most intriguing applications come from this field. As an example, the application calledMinthelps to track expenses and we are also allowed to see when we have to pay our bills. In addition, it also shows us how we could save money and we can follow the changes in our credit card. With the help of Mint we can easily create a budget too, or we can choose to follow the budget generated automatically by Mint for us. The automatically generated budget is based on our expense history.

Mint. Source: blog.mint.com/

Mint. Source: blog.mint.com/Another fascinating application is theFidelityapp. This application is intended for people participating in the stock market and it helps them to track easily and continuously how the market is changing, without taking out their phones in every two seconds.

Fidelty app. Source: https://www.fidelity.com/mobile/apple-watch/

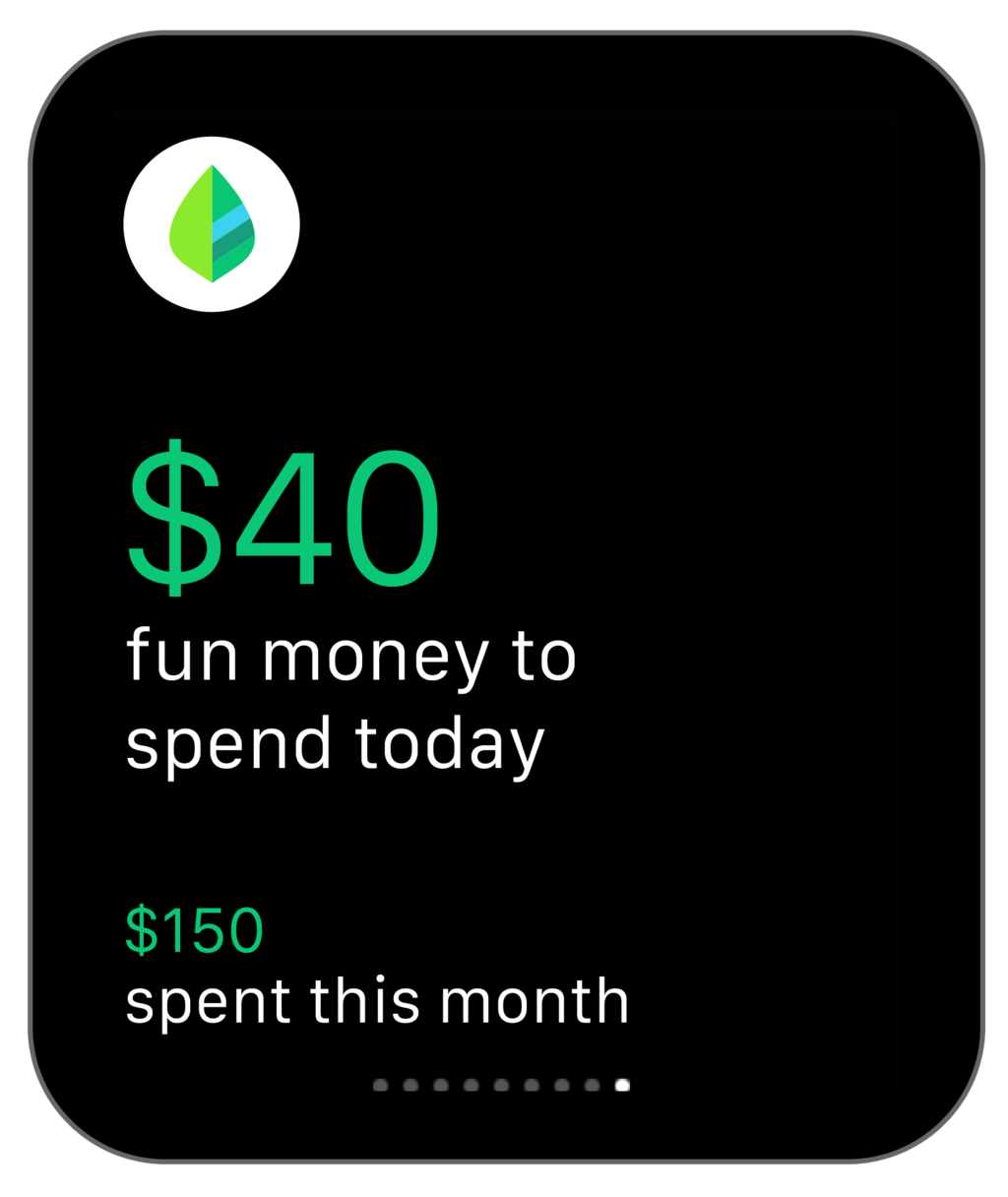

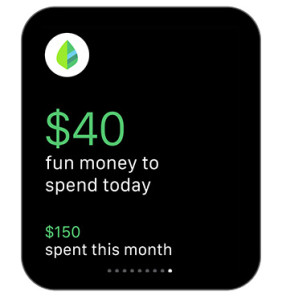

Fidelty app. Source: https://www.fidelity.com/mobile/apple-watch/A different type of Fintech app is thePennies.By the help of this application, we are allowed to set a budget for ourselves, we can document our expenses and we can track how much money we have spent. Furthermore, we have several viewing options: we can choose a daily/weekly or monthly view of our remaining balance based on our pre-set budget. Due to these options it is much easier to plan our financial future, our expenses and savings.

Pennies. Resource: https://www.getpennies.com/

Pennies. Resource: https://www.getpennies.com/Unspentprovides a similar service, with only a few taps, we can add new expenses/incomes to our budget. We canadd an individual budget we can easily keepwith the help of the application…except the period before Christmas, when everybody goes crazy with spendings.

Unspent. Resource: https://watchaware.com/watch-apps/unspent

Unspent. Resource: https://watchaware.com/watch-apps/unspent

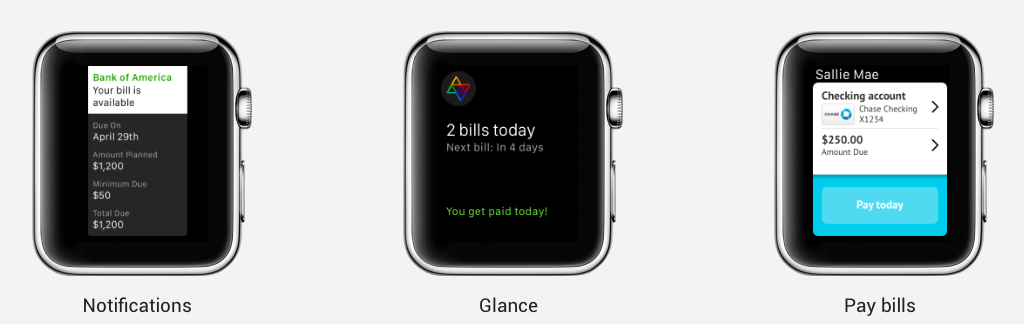

Prism– another application – makes it possible to pay our bills through its platform without additional costs for the transaction and without any delay. Moreover, the application also helps to have a nice overview of our balances.

Prism. Resource: https://watchaware.com/watch-apps/522138897

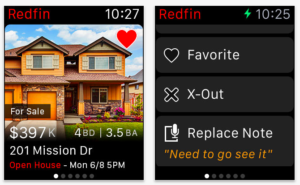

Prism. Resource: https://watchaware.com/watch-apps/522138897Real estate applications are fringing upon fintech. These applications allow users to see individual suggestions of real estates most of the time and by this way, they help users to find a suitable home. Redfin, for example is originally a real estate agency, but by recognising the need for online solutions, they created both mobile and smartwatch applications. These applications help users find real estates for sale in their area of interest (which can be setwithyour finger!). Beyond all these, the application also sends us notifications, whenever a relevant advertisement is added to the database. Finally, Redfin also helps us to arrange aviewing.

Redfin app Source: https://itunes.apple.com/us/app/real-estate-app-by-redfin/id327962480?mt=8

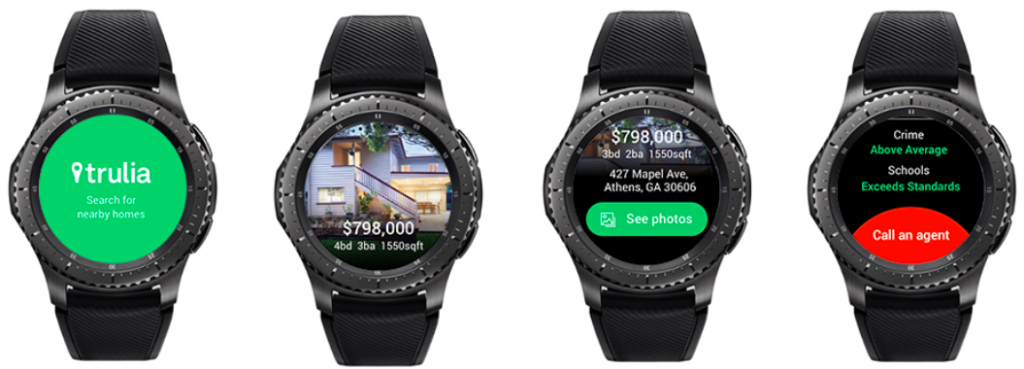

Redfin app Source: https://itunes.apple.com/us/app/real-estate-app-by-redfin/id327962480?mt=8One more example for real estate apps isTruliawith a similar functionality as Redfin has; it sends notifications to us about available homes based on our current location. We can also get additional information about the neighbourhood of the particular flat and other kinds of information such as crime rates, commuting time and other kinds of real estate market information.

Trulia. Resource: https://www.trulia.com/blog/tech/trulia-samsung-gear/

Trulia. Resource: https://www.trulia.com/blog/tech/trulia-samsung-gear/As a summary, we see that the bank sector is coming to the realisation that they must meet the modern world’s demands regarding technological advancements. As a consequence, we can see a rapid proliferation of financial applications both for mobile and for wearable devices. At the same time, however, we can also see that fintech projects independent of banks are almost always morecapable of innovating than traditional banks. Although banks have an immense knowledge and experience regarding financial processes and until this point the bank sector has monopolised the financial world, it is clear now that this monopoly has come to an end. The bank sector moves forward very slowly due to its isolation. Nevertheless, competitors outside of the bank sphere can adapt quickly and change freely since they don’t have such a strict regulatory system as banks usually have. Thanks – in a negative sense – to these circumstances, in essence, big banks are at a disadvantageous position within their own territory.

We don’t know exactly what the future holds in the field of financial applications, but either way, it is always advantageous when new actors appear in the market and they are challenging the ever growing bank industry.

About the authors

She has obtained a degree in Cognitive Science from Budapest University of Technology and Economics. She is currently interested in the fields of psycholinguistics, statistics and user experience research & design. Within UX research, her attention is captured by designing and evaluating user tests.

Related posts

Mobile banking in Austria

In Austria, which considered to be a rather conservative country, it is perhaps not surprising that people still largely prefer cash and traditional banking services to digital solutions. Nevertheless...

The Austrian Fintech scene - Greener grass?

From my earliest days of living in Hungary I was conscious that Austria played a big part in the history of my adoptive homeland. Austria was partner in a once-great empire, and a byword for high cult...

Sweden - Crypto and the International Vibe - part 1

Anders Norlin is the genial and well-connected Fintech advisor and former CEO of the Swedish Fintech member organization Findec, and he reports that a Swedish Fintech scene that’s ‘booming like crazy....

Related case studies

Percapita

We designed a full-fledged application for simplifying everyday finances.

K&H Bank's Corporate Netbank

The K&H Electra Netbank App consolidates all financial needs into a single, user-friendly application. With its intuitive design, businesses can effortlessly manage their company's cash flow, transactions, and investments from one centralized hub.

Atmen Fintech

Mobile App

Designing a Minimum Viable Product for a Diaspora Neobank Startup

Treasureup

We established written and visual consistencies and guidelines for TreasurUp’s financial platform.

Simple by OTP

Simple by OTP Bank is Hungary's No.1 mobile payment app for cashless payments with 1M+ downloads, and 1 million+ transactions.

White Label Banking App

We provide full-blown next-generation mobile banking solutions for sales-oriented banks.

Want to read more

about UX, fintech and banking?

Subscribe to our biweekly newsletter and get the latest of our news and thoughts!