The Danish Fintech Scene - Trust, Design, and something much more

Well, no actually, the Head of Relations and Global Events for Copenhagen Fintech was talking about a real boat, as if no self-respecting Fintech organization would be without one. When the photographic evidence arrives later in the day I see that Fintech & Dreams - as the boat is named - won’t be making Jeff Bezos envious, but I’m still impressed by Fintech-ers holding meet-ups on the Copenhagen waterfront, in their own boat.

“Considering it’s relatively small size there are so many good things happening with Fintech in Denmark,” Sarah says. She points to the considerable success of two-times unicorn Chainalysis which provides blockchain data and analysis to government agencies, banks, and businesses around the world. Founded in 2014, by March 2021 Chainalysis had raised $100 million in an investment round valuing the company at $2 billion, which is now headquartered in New York.

Sarah Millerton

Sarah MillertonSarah is in fact Swedish, and when travelling to the office does so from Malmö. Driving across the Øresund Bridge linking Sweden and Denmark gives her time to think and prepare, in this case for sharing her thoughts about Fintech: “Everything is digital here. The Nordics are all digital and there is widespread trust in technology. We have apps on our phones for healthcare, social benefits, payments, sharing costs... We have Swish and MobilePay, and I never need cash. In fact my son is eleven and he’s never used cash!”

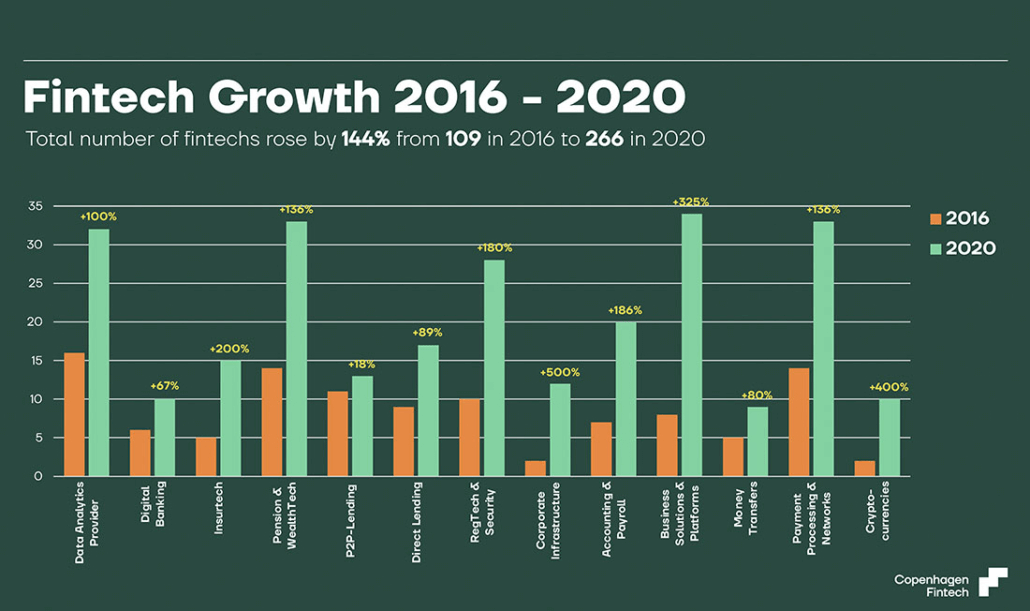

144% growth

So the adoption of Fintech is ‘normal’ and straightforward in Denmark, and this comes together with other trends. One is a long tradition of high quality design, across all aspects of life, with a very human-centric approach. “Denmark is a design country,” says Sarah. She also points to the public awareness of sustainability issues and ecological impact, and how this connects with Fintech startups.

So the scene is vibrant, and Fintech is well-accepted.

The steady rise in Copenhagen Fintech activity

The steady rise in Copenhagen Fintech activity“In our Fintech Lab we have around 40 companies with a strong physical presence, and we put together around 200 events a year, as well as the largest Fintech Conference, during Copenhagen Fintech Week,” Sarah continues. “There were 170 global speakers at the last one. We have mentor schemes for startups, and there are more and more mature unicorns. Part of our mission is also to attract international startups to Copenhagen, and since we began in 2016 the Fintech scene around the city has grown by 144%. Copenhagen Fintech is the glue and matchmaker between corporates, regulators, investors, incumbent banks and startups.”

I want to know, why Copenhagen Fintech, and not Fintech Denmark? Sarah says that Copenhagen Fintech is very much a Nordic hub, and in the Nordics it was simply easier to make it clearly recognizable as Copenhagen. There are also smaller cities with a high focus on specific startups.

Post interview, Sarah is also keen to make sure I understand that, “We in the Nordics are fiercely proud and fight for gender equality.” There are relatively few women active in Fintech to date in Denmark (and indeed across Europe), so that particular fight has a long way to go yet. For a bit of background, I check in with the figures for the Folketinget - the Danish Parliament - and see that of the 179 members, a steady figure of around 70 are women. That’s way more gender-balanced than many countries, but with still a way to go. (I make a note-to-self to explore this more, because why are women so under-represented in an industry where there is no reason for this to be the case?)

Simplifying life

Sarah mentioned using MobilePay, which makes the claim, ‘We simplify life’, so let’s check in next with Peter Gregersen, Chief UX Designer for the company, which started life in 2013. He echoes Sarah’s observation of the widespread Danish digital experience: “We operate in a Nordic context where users are ready for digital products. We could see that with the introduction of mobile banking, people had an app for checking their balance. But the payment between people - P2P - was actually quite cumbersome. You would need an account number, and you would need to ask for that, even if a friend was a customer within the same bank. So we tried to solve that by basically continuing the mobile banking journey with MobilePay, to make payments easier. MobilePay isn’t a new invention, because it uses well known components, like a bank account, a phone number, SMS, and so on. It’s smartphone technology.”

And it took off.

MobilePay

MobilePayIn the first year of the launch by Danske Bank, MobilePay was downloaded more than a million times. A year later, with added functionality and users in Finland as well as Denmark, the app was widely usable in shops, webshops, and at supermarket checkouts. ‘MobilePay’ was even declared ‘Word of the year’ in Denmark.

By 2016 other partner banks in Denmark were joining the ecosystem, and a sister app called WeShare was created, originally to aid homeless people selling a newspaper on the streets. By 2017 the milestone of a million transactions in one day was reached, with the following year seeing 4 million users signed up to the app. (And if you’re wondering how a country with a population of 5.8 million could have 4 million users, by this time MobilePay uptake was spreading around the Nordic area, with Greenland also coming on line in 2020).

Today the dominance of MobilePay is notable: 5.8 million users, with 60-plus partner banks and 200,000 shops and webshops accepting MobilePay. 90% of Danish smartphones have the app installed, and 18 billion euro was spent with MobilePay in 2020. This is quite some Fintech success story.

Peter Gregersen

Peter GregersenTrust, and fighting for the User Experience

It might have been very different, as Peter Gregersen explains, “One funny thing around MobilePay is that Danske Bank was part of a joint venture with other banks in Denmark, to build this product. But the point was reached where we backed out because we felt it was going too slow. We were scared that the overall user experience could be compromised, so we took the decision to build it ourselves, because we wanted to ensure it could be done as simply as possible.”

I wonder if at that point there wasn’t the temptation to go ahead as entrepreneurs, and design the app without banking support. Peter laughs, “Actually, the team joked that we could just as well have been sitting in a garage and doing the exact same thing! But we were growing out of a bank and relying on the trust we had with the bank. Besides that, we were able to use the bank infrastructure to build the product. We did the analysis in the beginning: Should we build it from scratch? Or should we rely on the bank infrastructure, which basically was mainframes from the 70s? We decided to rely on the latter to build it, but putting a new smartphone solution on top of the mainframe gave us incredible headaches!

I recall a lot of arguments and discussions on how to build the right thing and not compromise the user experience.”

Aha, the UX factor! Example please?

MobilePay's office

MobilePay's office“One example is that we wanted to introduce a solution where you could request money, the opposite of sending money. We wanted to have that in the first release, in order to onboard new users and have them spread the word organically. That was a pain to build on a mainframe solution designed for banking transactions. But the good thing about it was that scaling the solution was then very easy. So right from day one, we were able to scale quite quickly without any problems. And if you look at the numbers today, we have the entire population on board in Denmark, with 95% of all Danes being users of our system. It's kind of a national infrastructure, and we were only able to get that many users on board because we had the banking infrastructure. So we’ve had really rapid growth. At least that was one advantage of being part of a bank!”

Starting from a blank sheet of paper

Peter’s description of the genesis of MobilePay, wrestled from a multi-bank design process that seemed doomed to failure, and then built on top of legacy systems certainly sounds like a ‘headache’, despite MobilePay’s ultimate triumph. But let’s take a look at what happens when you start instead from a blank sheet of paper.

Lunar's office

Lunar's office“The Human Computer Interaction (HCI) Wave was contributed to massively by research at Aarhus University in the 80s and 90s. The University brought about some really great things in terms of qualitative design and participatory design,” he says. “So it's part of my educational background.”

Kasper agrees with the point made by Sarah Millerton that there is a strong design consciousness in the Danish population at large. “Your average users have high expectations in terms of user experience, both functionally and aesthetically. That’s rooted in our design culture that goes beyond digital products. I believe design traditions influence Scandinavian people's expectations of what they see and how things should work. It's paramount to our user base.” Kasper quotes Steve Jobs: ‘The design is not just what it looks like and feels like. The design is how it works.’

Kasper Mathias Svendsen

Kasper Mathias SvendsenLunar landing

So what about the prominent pitch made by Lunar Bank to potential customers that the neobank is ‘Your other bank’? I put it to Kasper that usually new banks are eager to prove their ability to replace incumbent banks. Doesn’t Lunar want to migrate users to the platform?

“It isn't really important to us,” Kasper says. “80% of the Scandinavian population has never tried more than one bank. We get our bank from our parents and their parents before them. And even though there's a growing dissatisfaction with the banking system, we just stick with it. You can have your entire spend universe with Lunar, utilizing our features to get a great overview of how you use your money to save, spend and invest, and you can still stick with your old bank. For most people, it's a necessary evil to have a traditional bank. We want to do it differently - we want you to go into our app and interact.”

OK, so customers interact, and then what? Lunar is a new bank, and it’s attracting younger people. One of the areas of interest is in investment, but that’s also one bogged down in difficult terms and complicated language. Lunar has put out the challenge to create simple, clear investor-friendly ‘universes’ that will encourage younger people to start investing.

Then there’s Lunar’s rounding up feature…

I remark to Kasper that I’ve never heard of a bank which deliberately gives clients inaccurate figures, but he explains the concept. It’s a sort of savings-by-stealth program where if - say - a user spends 49.8 krone on a purchase, it’s rounded up to 50 krone. So by very small degrees, a user is saving up, without even being aware of it. It’s a ‘digital coin jar’ and Kasper says it’s one of Lunar’s most beloved features.

Environmental consciousness

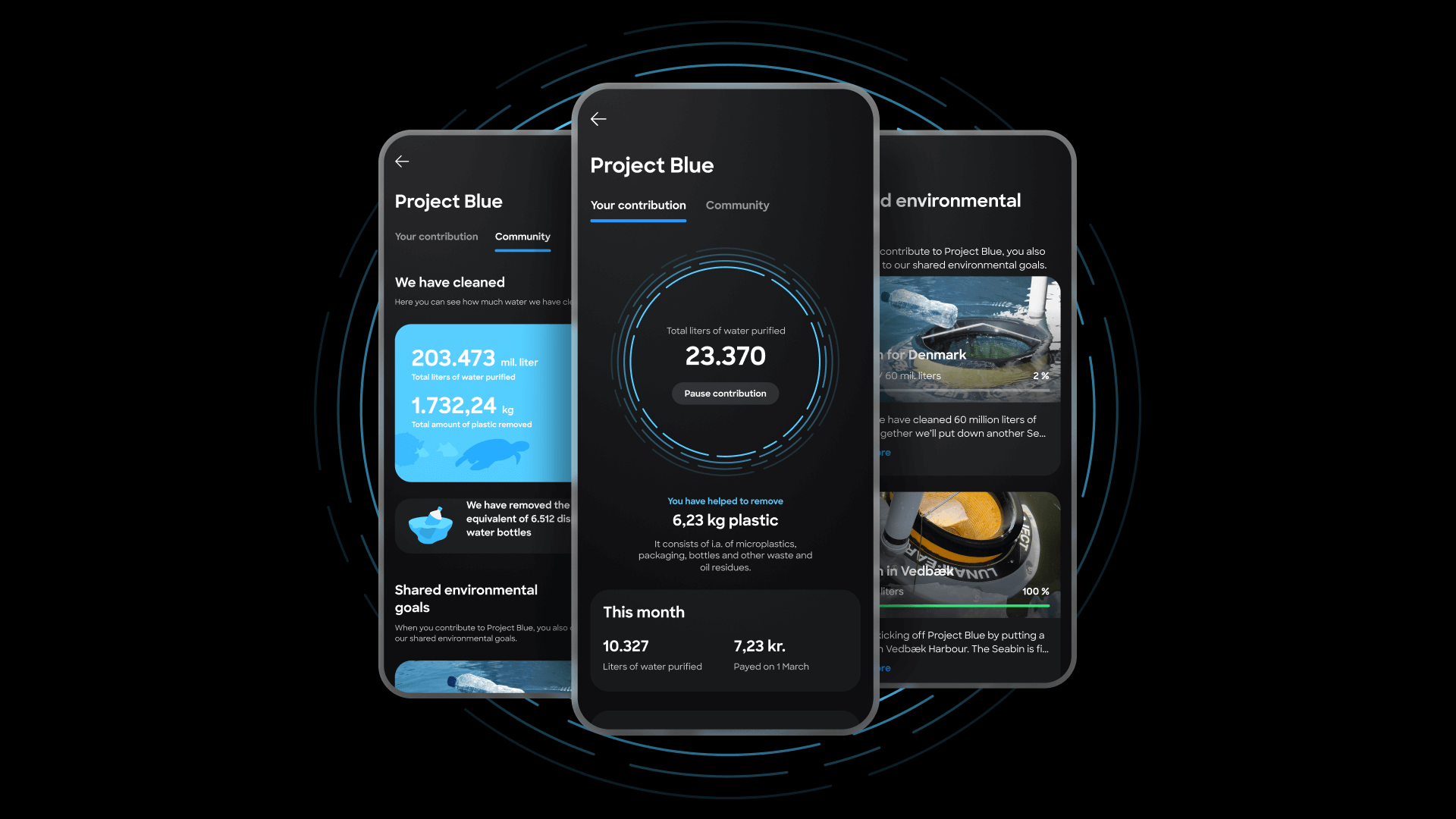

Another eye-catching initiative is the Project Blue ocean cleanup project where a user’s Lunar card spending helps remove plastic waste from the Nordic oceans, using ‘Seabins’.

Seabin ambassador and Olympic athlete Lin Cenholt

Seabin ambassador and Olympic athlete Lin CenholtKasper is personally involved in this, and when Lunar was deciding what project to support, he went on the streets to talk with as many people as possible about what mattered to them environmentally. He offered three projects - the tracking of CO2 levels, reforestation, and ocean clean-up. An overwhelming 90% responded in favor of the ocean cleanup. “It's a very easy problem to understand - it's very tangible. You can see it, and feel you can make a difference, whereas CO2 levels are a bit more difficult to grasp. Planting trees also has a bit of a bad rep, in terms of who's doing it, and where they're doing it. Just preserving forests that were not meant to be cut down doesn’t seem so great. But with ocean cleanup we hit the nail on the head.”

Project Blue's interface

Project Blue's interfaceTesting, testing, testing

András Rung of Ergomania is on our call and wants to know about the Lunar design work, and how this can be assessed from the user’s point of view. Kasper responds that this is one of the most challenging things in the hyper-growth phase that the bank is undergoing. The learning process is vital, he says, with testing, testing… and testing.“We make a kickoff as quickly as possible, creating some sort of common visual language - most often wireframing a mixture of low and high fidelity prototypes - so we have something that we can use internally to align, and get into the hands of people. From our workshop day onwards, we have something that exists with our users, in a maximum of a week. It's all about getting out all those great thoughts, functionality flows, everything in order to be able to test an idea.

I think what we do is very common, and you need to do that no matter what industry, whether you're creating a product with an embedded screen or an app for banking activities. It's so crucial to get that first outside-in perspective very early on. We think a lot about what kind of processes or tools to use, depending on the context, the user segment, and the product that we want to launch. We establish a framework for getting more qualitative data, or going into specific interviews, and observing our customers. We do that typically for one to two hours, just going over flows, having a specification ready, knowing what we want to address and be informed about.”

The design heritage

And do the resulting apps look Danish? Kasper laughs, explaining that Lunar is already also in Sweden and Norway, and so there is a shared design heritage. “Right now we’re focussing on the Nordics, and maybe they need something a bit different from Spain or Germany, but really good design works globally.”

“Denmark has a tradition of participatory design and listening to users and doing stuff in a simple way,” adds Peter Gregersen. “But overall you should expect that from any modern app from any modern company - that they would be designed with a high level of usability. It’s becoming more natural to everyone that when you launch a new product, it should be easy to use. I would argue that it wasn't like that 10 years ago.” And Peter adds that his design team are proud of the fact that they now get feedback from other UX-ers in other companies who are told that their work must be, ‘As easy as MobilePay.’ Another point of pride is that in 2019 Danes voted MobilePay as the one app they don’t want to be without (1% ahead of Facebook). As Peter says, “To me this is still strange that a payment utility can rank higher than a social media app that connects you to friends,” but he’ll take the accolade anyway.

Connecting all the players

Back with Copenhagen Fintech, I ask Sarah Millerton for an overall picture of the scene from where she’s sitting. She tells me that the largest sectors are Business Solutions and Platforms, with Payments and Data following up. The fastest growing categories are Corporate, and Crypto.

Some of the Copenhagen Fintech team in the Fintech Lab

Some of the Copenhagen Fintech team in the Fintech Lab“We need to support the whole of Fintech,” Sarah says. “If you only focus on one part you don’t have to be crystal clear, but we need to have a lot of knowledge across all of Fintech.” She cites regulations such as KYC as being increasingly important, and how vital it is for Copenhagen Fintech to be in touch with Regulators, helping reduce any friction with Fintechs - particularly startups. She makes the point that greater regulation is a two-edged sword because while it can make life harder for the Fintechs, it also increases trust with consumers.

At the same time, Sarah observes that convenience is also an important feature for consumers and points out the case of Klarna Bank, which has over 80 million users in the Nordic countries. In May 2021 the Bank had a major security outage where users were able to see the details of other accounts including personal information, address, purchases, and payment methods. Despite this major breach, Sarah remarks in follow-up notes, ‘I don’t believe they actually lost very many customers, because they make payments so much easier for the consumer.’

So trust is important, yes… but even when that trust is eroded, consumers have become familiar with the ease-of-use of banking and financial apps and are - apparently - willing to forgive even major outages for the sake of convenience.

Meanwhile many Danish Fintechs are focused on B2C solutions that help ease consumer pain, so anything that encourages consumer trust is helpful.

Copenhagen Fintech also has the ability to facilitate discussions between corporates, regulators, and Fintechs to make new things happen. This includes helping make Fintech an economic stronghold for Denmark, and pushing important agendas for Fintechs, such as the urgent need for more talent in Denmark. A May 2021 initiative draws attention to nine key areas, including a talent sharing and lending program between established companies and Fintech startups; improved training in Fintech competencies; and the training of Fintech talents from developing countries - along with encouraging diversity.

A headache for innovation

The regulatory engagement Copenhagen Fintech is involved in is also on Peter Gregersen’s radar: “Basically, we are running on the same legislation across Europe. At least, that's how it should be. But the thing is, governments interpret EU legislation differently. So I would say that it's getting tougher to defend good user experience, because we are facing these heavy legislation requirements. One example is PSD2 with strong customer identification on each transaction: that was hard for us. The thing with mobile is, you log on and then you're able to perform your transaction without any further kind of authentication. We were required to change that, and it’s just one example of how legislation is pushing the user experience. If we were to launch more payment solutions today with the same legislation, you could forget about it, because everything is so strict right now. That's a headache for innovation.”

Ones to watch

As Peter Gregersen mentioned, prior to MobilePay, P2P payments were ‘cumbersome’ and Sarah Millerton recalls the same thing. Coming from an incumbent banking background she is conscious of how little day-to-day life was helped by the old order of things.

So are there any new ‘ones to watch’? Sarah says to check out Tjommi, a Norwegian startup that went to Copenhagen for one of the association’s programs, and stayed. The app is very consumer-focussed, promising to recover the difference if the price of your purchased goods drops after purchase, saying: Get your money back with Tjommi. It only takes three steps:

- Sign up with your mail

- We'll get receipts from your inbox and track the prices of your products

- If the price drops, we'll get money back from the store! Get your money back now!

On a different scale to Tjommi, another one to watch is Kompassbank, which completed a $22.5 million Series-A funding round in March 2021 - a challenger bank to the challenger banks such as Lunar.

And speaking of Lunar, what’s the story with the cute cartoon rocket that is sometimes featured in the neobank’s marketing? “I guess I should know that shouldn’t I?” Kasper Svendsen laughs. “It’s the final frontier, no boundaries. In banking, people talk about ‘Moonshot Projects’, meaning something that’s very innovative, which may or may not succeed. Our founders conceived of Lunar as a moonshot project, and we use the term internally: ‘We’re building a rocket, welcome aboard the rocket ship!’ Now we're in this hyper growth space, where everything is moving along really quickly, and everybody has to be on their toes to pitch in and make it happen. This is a very busy and demanding period, but it’s also very exciting.”

Kasper adds that when he went to his first interview with Lunar, he wasn’t even particularly interested in taking a new job, but was attracted by ‘the startup vibe’. It’s a vibe that he now seems very engaged by.

Simplicity is vital

Peter Gregersen also comments on the flat organization of MobilePay which he describes as ‘typically Danish’, where Design has a high degree of impact, especially true at the beginning of the MobilePay journey. However, “With new features, it's more like a combination of us giving input to the business case. It's kind of a puzzle to do that in a company like ours because we are in a position where we are not allowed to make any mistakes. Operational focus is really high and there’s a relationship to that when you're developing new features. It's hard to balance between new features and simplicity.”

He sees Revolut as an example of initial simplicity which has developed increasingly complicated navigation, and - in Peter’s opinion - somewhat lost it’s way by becoming too ‘cluttered’. “Revolut is still a good application, but it has more weaknesses than three years ago. We face the same problem: Everyone wants the newest feature on the top page, and we have to sometimes fight to defend our position. So the MobilePay top page hasn’t changed all that much.” In fact sometimes Peter and his team make the decision, ‘Great feature… but it doesn’t belong here.’

So which Fintechs have caught Peter’s eye as being best in class? He points to Spiir, which - according to the website - ‘Started with a simple question: Who says personal finance has to be boring?’

The company has been up and running since 2011, ‘Helping more than 400,000 people in the Nordics get a better grip on their finances without having to struggle with old-school budgets or boring spreadsheets.’ Also of interest is Aiia, a sister company to Spiir, selling access to aggregated PSD2 data: ‘A single API that connects you to all the Nordic banks and gives you accounts and transactions data from real users. All you have to focus on is building new digital services that benefit you and your customers.’

Peter is also complimentary about Lunar Bank and refers back again to simplicity being a keynote of all good design - and not only in Denmark!

Kasper Mathias Svendsen says Lendify is interesting because it’s a peer-to-peer lending platform. It’s a Swedish Fintech which was acquired by Lunar Bank, and the company says of itself: ‘Lendify caters to Swedish households…’ (and soon other Nordics) ‘...with high credit ratings who often already have loans from one of the traditional banks, but can and want to get better terms. Lendify’s goal is to give borrowers fair conditions with lower interest rates and savers higher returns.’

Lendify

LendifyHej hej

Before saying Hej Hej and leaving Peter, Sarah and Kasper, I try for a few personal reflections: Who is a mountain biker, or who writes poetry in their spare time?

Peter admits to a keen interest in garden design, which he says, “Like software has no end - the garden will be even nicer next year!” He also offers an extra insight on interesting technological developments that are tweaking his interest: “One funny technology that we're looking at right now is QR code. That's actually kind of old fashioned, but the thing is that we have been running point-of-sale solutions for a lot of years, based on Bluetooth Low Energy technology, where you would pair your phone to a terminal in the shop. And we did that using BLE, because Apple had blocked the NFC (Near Field Communication) chip to anyone else. So we needed another technology, and right now we are getting to where we're not able to develop BLE further. So we are putting our bets on QR codes instead. It’s more of an old fashioned technology, but we see from China that it's huge. So we have a strong belief in that.”

Sarah Millerton is an abstract painter (with work in the Saatchi Gallery, London), when not looking after the ever-expanding interests of Copenhagen Fintech, about which she radiates optimism: “I’m super-positive because I can see how much is happening here in Copenhagen. And right here in our physical space it’s very exciting. I’m delighted to see new startups. I believe we’re on the brink of something much more.”

Kasper Mathias Svendsen says that family, with two kids under ten and a newly-acquired puppy pretty much make him a ‘full-time father’, but he offers a reflection on the Lunar experience: “It's not every day you get to be part of building a bank from scratch. In just the past couple of years we have achieved what the incumbent banks spent hundreds of years building.”

Two recurring themes have run through this brief story of Fintech in Denmark. There is Trust, with the importance of all sides being open and clear. The other consistent factor is the importance of great Design.

And with Danish Fintech growing and growing, perhaps that famous line from the movie Jaws also applies: “You're going to need a bigger boat!”

Fintech & Dreams

Fintech & DreamsAbout the authors

Harlan Cockburn is a writer and director based in Budapest, Hungary.

Related posts

Aron Bijl - Ergomania Senior UX Designer

If you get into conversation with Aron Bijl, be prepared to cover a lot of ground. When we speak he’s in a family home outside of Budapest, and we’re quickly ranging over subjects as varied as why it’...

The Bulgarian Fintech Scene - Dedication and tough work

For me, one of the joys of interviewing Fintech players around Europe is the random and sometimes fascinating stories which surface. One such story comes to light in talking with Georgi Penev, Directo...

More Popular Than Expected: The Secret of The Best Voice-user Interfaces

Personal assistants communicating with the VUI, or voice-user interface, have become much more popular than the largest industry players expected them to be. Amazon, Microsoft, Google, or Apple all ha...

Related case studies

Percapita

We designed a full-fledged application for simplifying everyday finances.

K&H Bank's Corporate Netbank

The K&H Electra Netbank App consolidates all financial needs into a single, user-friendly application. With its intuitive design, businesses can effortlessly manage their company's cash flow, transactions, and investments from one centralized hub.

Atmen Fintech

Mobile App

Designing a Minimum Viable Product for a Diaspora Neobank Startup

Treasureup

We established written and visual consistencies and guidelines for TreasurUp’s financial platform.

Simple by OTP

Simple by OTP Bank is Hungary's No.1 mobile payment app for cashless payments with 1M+ downloads, and 1 million+ transactions.

White Label Banking App

We provide full-blown next-generation mobile banking solutions for sales-oriented banks.

Want to read more

about UX, fintech and banking?

Subscribe to our biweekly newsletter and get the latest of our news and thoughts!